|

~

TRENDLines Research's

Covid Future Fatalities Projections

"future deaths" chart also viewable at: www.twitter.com/TrendlinesDotCa

& www.facebook.com/TRENDLinesResearch

next monthly chart update: June 6th 2023

|

OMICRON'S SUB-VARIANTS' GLOBAL WAVE HERE 'TIL JUNE 2023!

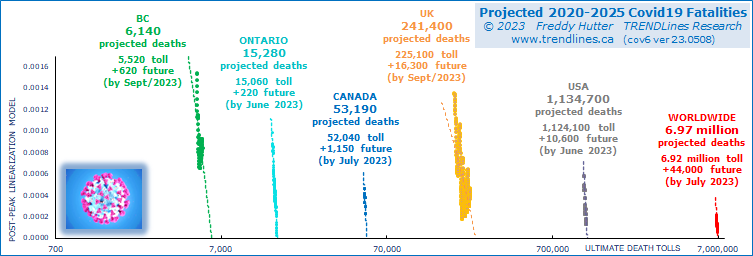

PROJECTED FUTURE FATALITIES: 44,000 WORLDWIDE

incl: USA 10,600 & UK 16,300 & CANADA 1,150 (incl 220 ONTARIO & 620 BC VICTIMS)

May 8th 2023 - Based on novel coronavirus's ever-changing

mortality rate in recent weeks, today's update

of TRENDLines Research's

Covid-19 fatalities

model projects an ultimate 2020-2023 death count of 6.97

million worldwide (present toll 6.92 million + 44,000 future) incl 1,134,000 in the

USA (1,124,000 toll + 10,600 future); 241,400 in the UK (225,100 toll + 16,300 future) & 53,190

in Canada (52,040 toll + 1,150 future) incl 15,280 in Ontario (15,060

toll

+ 220 future) & 6,140 in BC (5,520 toll + 620 future) - based on

current relaxed policymaker mitigation of the Omicron BA2/4/5, BQ1 & XBB1 sub-variants.

Whereas

previous lethal coronavirus events (MERS & SARS) were relatively

short-lived due to aggressive contact tracing, misguided policymaker mitigation decisions allowed Covid-19 to become

a multi-wave pandemic with a projected 43 month start-to-end duration (assuming no new variants-of-concern).

This humankind

disaster stems

from most jurisdictions: (a) adopting the horrific Trump strategy of

prematurely lifting restrictions (thrice or more); (b) reluctance to

require/maintain shelter-in-place; (c) an over-reliance on

vaccination programs; (d) failure to assist vaccination in

developing nations; (e) identifiable

leadership complicity in anti-mandate campaigns (eg masks, testing, social distancing &

vaccinations); & (f) virtually abandoning vigilant testing &

contact tracing convention post Delta.

note: text below reflects June 30 2022 Report

- balance of text will updated later this month!

- see archive of past projection in table below

These

failures to isolate the original virus led to successive

surges of same and provided opportunities for spawning Alpha, Beta, Delta & Omicron

(incl BA2/4/5) variants-of-concern to flourish. Modelling

reveals this event

should have been only a mere six-month episode with 1.1 million

fatalities.

Instead, policymaker hubris may have

caused 5.3 million unnecessary victims worldwide. These surplus

deaths include 870K in USA, 149K in UK & 29K in Canada (incl 10K in

Ontario & 2,900 in BC).

My Post-Peak Linearization Model indicated prudent mitigation

efforts had essentially suppressed Covid's first surge by mid-2020 in

the UK & Canada (incl Ontario & BC.

Unfortunately, those early lock-down & shelter-in-place sacrifices proved to be in

vain. Premature relaxation

of Orders and restrictions in all four jurisdictions gave rise to new

surges upon each

attempt at re-opening. Similarly, just as the USA & Global models were to

signal suppression in July 2021, the Delta wave overwhelmed the suppression progress.

In much of the world,

similar policymaker mismanagement resulted in a string of five waves

(defined as

seasonal outbreaks or material strain mutations): Covid19 original strain,

Alpha/Beta, Delta, Omicron & its BA2/4/5 sub-variants and surges within

those waves.

As a "post-peak" model, no

projections

were generated during the strong Delta & Omicron episodes.

Surges in cases, hospitalizations, ICU and deaths since mid 2021 reigned

primarily in vax-hesitant regions. Excepting developing nations

lacking vaccination access, one might surmise there was a lot of

Darwin's natural selection at

work - and fortunately - victims were/are mostly right-wing qAnons.

Originally, consensus held

natural & community (vaccinated) herd immunity would

kick

in upon regions attaining 67% infection and/or jabs. But failure

to suppress the original strain and the subsequent spawning of

variants-of-concern, broad-based vaccine hesitancy & the inability

of vaccines to prevent break-thru cases upon waning immunity appear to

have killed off any hope of illusive herd immunity.

Current

model runs indicate Omicron's sub-variants will transition to endemic

status (health sector no longer overwhelmed) over the coming weeks and

months. In early June 2022, the UK became the first of our six

tracked jurisdictions to attain endemicity. Covid related deaths

should wind down by late July in the UK; by September in

Ontario; October Canada-wide; March 2023 in BC; & June

2023 in the USA. However, with 33% of the globe still lacking even

a first jab, it is

highly probable new variants-of-concern will arise this Autumn.

See website table for archive of all my projections since April 2020. The model's composite chart, underlying stats

& analyst commentary (by Freddy Hutter) are updated monthly at:

www.trendlines.ca & chart only at www.facebook.com/TRENDLinesResearch

& www.twitter.com/TRENDLinesDotCa

WORLDWIDE analysis

Based on existing lax policymaker mitigation and mortality

trends in recent weeks, the TRENDLines Post-Peak Linearization Model

projects Omicron's sub-variants (BA2/4/5) will claim yet another 98,000

fatalities

across the

globe as the present wave expires in February 2023. Added

to the current toll (6.322 million), an ultimate 6.420 million victims are projected over 2020-2023. Today's

daily-deaths rate (1,400) is down 90% from its January 2021 record high

(14,400). Today 63% of the world's population have at least one

jab. Future variants-of-concern may inflate final numbers.

Troubling as today's ultimate

projection may be, the alternative natural herd immunity strategy promoted

by conspirators would have cost 102 million lives (7.6 billion x 67% x

2.0% Alpha/Beta case fatality rate) and with no guarantee of permanent immunity.

The

10 nations with the highest daily-deaths rate today: USA (260),

Brazil, Taiwan, UK, Russia, Australia, France, India, Chile

& Canada.

The model reveals 5.2 million souls (of 6.4 mil total) will have

perished unnecessarily due to misguided policymaker decisions to

prematurely re-open.

41% of worldwide victims resided in long-term care facilities.

Worldwide mortality rate: 0.08% or 813 deaths/million population

USA analysis

The

model similarly projects Omicron's sub-variants (BA2/4/5) will claim yet

another 24,400 fatalities across America as the present wave expires in June 2023 -- based on existing policymaker mitigation. Added

to the current toll (1,025,900), an ultimate 1,050,300 victims are projected over 2020-2023. Future variants-of-concern may inflate final numbers.

Today's daily-deaths rate (260) is 93% below its Jan/2021 record high (3,500). The States with the most daily-deaths today

are Florida (60), California, Georgia, Pennsylvania, New York & Texas.

Troubling as today's ultimate projection may be, the absurd natural herd immunity policy promoted by the Trump White House would have cost 3.9 million American lives (327 million x 67% x 1.8% Alpha/Beta case fatality rate) with no guarantee of permanent immunity.

During a White House Rose Garden

virtual town hall on

March 25th 2020, the former President proposed packing the nation's churches on

Easter and return to work the following day. It was on this

precise day America

was infected with "the TrumpVirus". On that day the USA had

only 4% of global Covid deaths - apropos considering the nation has 4% of the

world's population.

It marked the day everything

changed. For context of Trump's containment failure, the USA had over

half of worldwide cases & deaths in 2020. Twenty-six months later,

the USA still has 16%

of world's cumulative Covid

cases, 16% of the today's global "active" cases & 16% of worldwide body bags. The uncontained TrumpVirus resulted in GDP crashing at a historic -31%

pace in 20Q2. 75 million workers initiated unemployment claims due to the

pandemic during his term.

The President caused a TrumpVirus resurgence only for the purpose of salvaging his legacy. He

desperately wanted to avoid voters going to the polls realizing The Donald (alone)

was at fault for April 2020's 22% U-6 Unemployment Rate & plunging

the U.S. economy into its deepest crash (-31% GDP) ever - including the Great Depression.

The model reveals reveals 870,000 souls (of 1,050,000 total) will have perished unnecessarily due to

misguided policymaker decisions to prematurely re-open.

Long-term

care residents comprise 1% of the USA population but were 36% of

Covid19 victims - as high as 73% in some States. 81% of fatalities

were over the age of 64 and 95% were over 49.

USA's mortality rate: 0.30% or 3,009 deaths/million -- 17th worst in world - behind

Peru (0.66%), Bulgaria, Bosnia-Herzegovina, Hungary, Georgia, North

Macedonia, Croatia, Czechia, Slovakia, Romania, Moldova, Lithuania, Brazil, Slovenia, Poland & Chile.

UK analysis

The model

projects Omicron's sub-variants (BA2/4/5) will claim yet another 680 fatalities

across the UK as the present wave expires in late July -- based on

existing lax policymaker mitigation. Added to the

current toll (199,420), an ultimate 200,100 victims are projected over

2020-2022. Future variants-of-concern may inflate final numbers.

The UK's

wave#1 was initially suppressed back on Aug 2nd 2020 - when new daily

cases

sunk below 750 and daily deaths were down to single digits. The model

deemed wave#1 suppressed a second time (late May 2021) when once again

daily-deaths hit single digits. Today's daily-deaths rate (29) is 98% below its Jan/2021 record high (1,250).

Troubling as today's ultimate

projection may be, the alternative natural herd immunity strategy promoted by conspirators would have cost 757,000 UK lives (66 million x 67% x 1.7% Alpha/Beta case mortality rate) with no guarantee of permanent immunity.

The model reveals 149K souls (of 200,100 total) will have perished

unnecessarily due to misguided policymaker decisions to prematurely

re-open.

The

UK comprises only 1% of global population but has 3% of the Covid19

deaths (down from 11% in 2020) and 4% of today's world "active" cases.

37% of victims lived in long-term care homes.

UK's mortality rate: 0.26% or 2,555 deaths/million (28th worst in world)

CANADA analysis

The model

projects Omicron's BA2/4/5 sub-variants will claim yet another 730 fatalities

across Canada as the present wave expires in October -- based on

existing lax policymaker mitigation. Added to the current toll (41,570), an ultimate 42,300 victims are projected over 2020-2022. Future variants-of-concern may inflate final numbers.

The model reveals Canada's wave#1 was initially suppressed on Aug 7th 2020 - when new daily cases

sunk below 350 and daily deaths were down to single digits. Today's daily-deaths rate (20) is 89% below its May 2020 record high (176).

Troubling as today's ultimate projection may be, the alternative natural herd immunity strategy promoted by conspirators would have cost 421,000 Canadian lives (37 million x 67% x 1.7% Alpha/Beta case fatality rate) with no guarantee of permanent immunity.

The model reveals 29K souls (of 42,300 total) will have perished unnecessarily due to

misguided policymaker decisions to prematurely re-open.

Canadian

media (CTV & CBC) annually expose nursing home neglect

and under-staffing, so there's no

surprise this sector saw the most confirmed cases. 69% of Covid19

victims resided or worked in long-term facilities. 88% of

fatalities were over the age of 69.

Canada's mortality rate: 0.10% or 1,021 deaths/million

ONTARIO analysis

The model projects Omicron's BA2/4/5 sub-variants will claim yet another 81 fatalities across Ontario as the present wave expires in September -- based on existing lax policymaker

mitigation. Added to

the current toll (11,873), an ultimate 11,954 victims are projected over 2020-2022. Future variants-of-concern may inflate final numbers.

It reveals Ontario's wave#1 was initially

suppressed on July 7th 2020 - when new daily cases

sunk below 150 and the Province reported its third consecutive

fatality-free day. Today's daily-deaths rate (3) is 96% below its record highs (62) in May 2020.

Troubling as today's ultimate projection may be, the alternative natural herd immunity strategy promoted by conspirators would have cost 171,000 Ontario lives (15 million x 67% x 1.7% Alpha/Beta case fatality rate) with no guarantee of permanent immunity.

The model reveals 10K (of 11,954 total) will have perished unnecessarily due to

misguided policymaker decisions to prematurely re-open.

Finding 66% of its Covid deaths in nursing homes, to Ontario's credit it was one of the first jurisdiction to initiate an

Inquiry Commission to evaluate the crisis in long-term seniors care

facilities.

Ontario's mortality rate: 0.09% or 852 deaths/million

BC analysis

The model

projects Omicron's BA2/4/5 sub-variants will claim yet another 319 fatalities

across the Province as the present wave expires in December -- based on

lax existing policymaker mitigation. Added to the current toll (3,722), an ultimate 4,041 victims are projected over 2020-2022. Future variants-of-concern may inflate final numbers.

It reveals BC's wave#1 was initially

suppressed way

back on June 20th 2020 - when new daily

cases had dwindled to single digits and the Province reported its ninth

consecutive fatality-free day. The

model deemed wave#1 suppressed a second time (late July 2021)

when once again daily-deaths hit single digits. And a third when Delta troughed in early January 2022. Today's daily-deaths rate (9) is down substantially from the record 21/day in December 2020.

Troubling as today's

ultimate projection may be, the alternative natural herd immunity

strategy promoted

by conspirators would have cost 33,500 BC lives (5 million x 67% x 1.0%

Alpha/Beta case fatality rate) with no guarantee of permanent immunity.

The model reveals 2K souls (of 4,041 total) will have perished unnecessarily due to

misguided policymaker decisions to prematurely re-open.

My

analysis of a Canadian Medical Assoc Journal study of Excess Deaths

(June 2022) indicates BC's ultimate Covid fatalities will, upon

reconciliation, be 8,000 -- not the 4K suggested by BC Gov't & CDCBC

official reporting.

This challenges BC's repeated boast of having among the lowest fatality,

mortality & incidence rates across Canada & the globe. But to their credit, while

British Columbia &

Washington State were the

first North American regions to see confirmed cases take off, wise

leadership quickly contained the spread -- before falling victim to

faulty re-opening strategies.

Further credit to BC in being among the first to mandate full vaccination for healthcare workers and bar

family visitations to nursing homes and disallow care workers from attending

multiple long-term residences. Residents of BC long-term facilities comprise 68% of total

fatalities.

BC mortality rate: 0.06% or 587 deaths/million

The TRENDLines Research POST-PEAK LINEARIZATION

MODEL (PPLM)

These six Covid19 projections are generated by TR's linearization

model. It extrapolates a jurisdiction's mortality rate after the curve's peak - particularly the most recent

days & weeks. The graph's data

points move left to right chronologically above its date's cumulative

death toll on the x-axis. The intersection (asymptote) of their

trend line at the x-axis indicates an estimate of the ultimate total

deaths. As daily data points are added, a

high y-axis data point (high mortality rate) will shift the bottom of the

trend line to the right

and a higher fatalities count ... and vice versa.

There is no medical component aside from tracking daily &

cumulative fatalities. This strictly mathematical model analyzes

nuanced gradient changes in

a curve's down-slope and assumes no change in gov't guidelines, orders

or citizenry behaviour. This same methodology has been

one of the criteria by which TRENDLines Research has determined global

& Saudi Arabia oil reserves since 2004. On request, I can similarly chart any Nation,

State, Province or Region - presented alone or with comparatives.

About TRENDLines Research

Data analyst Freddy Hutter of Vancouver Island BC has developed models

& methodologies for macro-economic charts & guidance for

policy-makers, stakeholders. legislators, investors, educators, and the

public with a

long term multi-disciplinary perspective since 1989. TRENDLines

removes the noise in (economic) data to reveal the underlying

trends. Specialties

include: Recession Indicators for Canada, USA & China;

Realty Bubble Indicators for Canada, USA, UK & Australia;

Global Oil Production & Price Component analysis/forecasts; &

national, provincial Party & Presidential political election

projections. Covid-19 ultimate deaths forecasting is the most

recent endeavour.

|

Archive of PPL Model's Projected 2020-2023 Covid19 Fatalities

|

|

BC

|

Ontario |

Canada

|

UK

|

USA

|

World

|

May 8 2023 May 8 2023

| 6,140 | 15,280 | 53,190

| 241,400

| 1,134,700

| 6.97 million

|

April 11

| 6,510 | 15,120 | 53,340

| 234,000

| 1,135,000

| 6.95 million

|

March 19

| 5,510 | 14,790 | 52,620

| 232,700

| 1,134,000

| 6.90 million

|

Feb 17

| 8,600 | 15,100 | 56,000

| 260,000

| 1,138,000

| 6.91 million

|

Jan 9 2023

| 7,900 | 14,280 | 55,400

| 232,400

| 1,215,000

| 7.50 million

|

Dec 10 2022

| 5,190 | 13,990 | 51,000

| 221,050

| 1,137,000

| 6.89 million

|

Nov 7

| 5,240 | 16,520 | 53,910

| 200,900

| 1,126,000

| 6.75 million

|

Oct 9

| 4,505 | 13,760 | 46,840

| 208,750

| 1,129,000

| 6.67 million

|

Sept 12

| 4,631 | 15,200 | 52,150

| 207,730

| 1,079,000

| 6.78 million

|

| Aug 21 | 4,281 | 12,940 | 46,400

| 208,260

| 1,085,000

| 6.67 million

|

July 31

| 4,050 | 12,390 | 43,470

| 201,270

| 1,076,000

| 6.60 million

|

June 30

| 4,041 | 11,954 | 42,300

| 200,100

| 1,050,300

| 6.42 million

|

May 20

| 3,564 | 13,790 | 42,270

| 200,200

| 1,027,200

| 6.36 million

|

April 8

| 3,066 | 12,750 | 38,470

| 195,650

| 1,015,000

| 6.33 million

|

March 6

| 3,196 | 12,810 | 38,050

| 163,180

| 1,071,000

| 6.31 million

|

February

|

-- Omicron variant surging in all 6 jurisdictions -- |

| January 2022 |

-- Omicron variant surging in all 6 jurisdictions -- |

Dec 18 2021

| 2,488 | 10,700 | 31,190

| 154,200

| 889,000

| 5.8 million

|

Nov 24

| 2,365 | 10,110 | 30,700

| 150,250

| 859,000

| 6.1 million

|

Oct 9

| 2,054 | 9,960 | 29,200

| 141,730

| 773,000

| 5.6 million

|

| September

| -- Delta variant surging in all 6 jurisdictions --

|

August

| -- Delta variant surging in all 6 jurisdictions --

|

July 5

| 1,778 | 9,800 | 27,020

| 128,990

| 621,000

| 4.4 million

|

June 2

| 1,807 | 9,440 | 27,490

| 128,435

| 655,000

| 4.6 million

|

May 3

| 2,257

| 8,600 | 25,820

| 128,200

| 650,000

| 4.3 million

|

April 1

| 1,668

| 7,965 | 24,070

| 127,460

| 584,000

| 7.7 million

|

March 1

| 1,406

| 7,270 | 22,840

| 127,100

| 570,000

| 2.9 million

|

Feb 3

| 1,317

| 7,680 | 22,260

| 129,500

| 520,000

| 2.7 million

|

Jan 18

| 1,250

| 7,810 | 22,700

| 102,700

| 604,000

| 9.0 million

|

Jan 2 2021

| 1,151

| 5,560 | 19,000

| 139,000

| 763,000

| 4.4 million

|

Dec 16 2020

| -

| 4,220 | 15,330

| 89,000

| 599,000

| 3.2 million

|

Nov 20

| -

| - | 13,400

| - | 396,000

| 2.1 million

|

Oct 20

| 412

| 3,540 | 10,800

| 46,500 | 295,000

| 2.0 million

|

Oct 10

| 374

| 3,540 | 9,840

| 44,450 | 289,000

| 2.1 million

|

Sept 30

| 290

| 3,038 | 10,160

| 44,800 | 270,000

| 1.7 million

|

Sept 20

| 437

| 2,947 | 9,895

| 43,840 | 266,000

| 1.7 million

|

Sept 10

| 277

| 2,905 | 9,440

| 42,200 | 245,000

| 1.4 million

|

Sept 5

| 274

| 2,909 |

9,460

| 42,120 |

267,000

| 1.4 million

|

Aug 30

| 216

| 2,929 | 9,450

| 42,230 | 284,000

| 1.4 million

|

Aug 25

| 217

| 2,868 | 9,370

| 42,010 | 269,000

| 1.5 million

|

Aug 20

| 205

| 2,862 | 9,302

| 41,990 | 265,000

| 1.5 million

|

Aug 15

| 204

| 2,851 | 9,100

| 48,600 | 418,000

| 2.1 million

|

Aug 10

| 207

| 2,852 | 9,075

| 48,800 | 377,000

| 2.5 million

|

Aug 5

| 205

| 2,854 | 9,070

| 48,500 | 282,000

| 2.0 million

|

July 30

| 207

| 2,845 | 9,050

| 48,200 | 308,000

| 2.0 million

|

July 25

| 199

| 2,843 | 9,030

| 48,100 | 239,000

| 1.6 million

|

July 20

| 215

| 2,850 | 9,060

| 48,100 | 204,000

| 1.5 million

|

July 15

| 200

| 2,825 | 8,940

| 46,200 | 180,000

| 1.1 million

|

July 10

| 189

| 2,820 | 8,930

| 46,000 | 175,000

| 1.2 million

|

July 5

| 180

| 2,845 | 8,910

| 46,000 | 173,000

| 1.2 million

|

June 30

| 177

| 2,890 | 8,840

| 45,600 | 161,000

| 1.3 million

|

June 25

| 172

| 2,920 | 8,860

| 44,700 | 141,000

| 1.2 million

|

June 21st 2020

Actual Deaths:

|

171

|

2,657 |

8,481

|

42,731 |

122,468

|

472,779

|

June 20 forecasts

for Year 2020

| 170

| 2,810 | 9,000

| 46,800 | 145,000

| 1,145,000

|

June 16

| 170

| 2,940 | 9,660

| 48,900 | 140,000

| 905,000

|

June 12

| 172

| 3,170 | 10,200

| 47,400 | 141,000

| 852,000

|

June 9

| 172

| 3,530 | 9,430

| 49,200 | 134,000

| 640,000

|

June 6

| 191

| 2,770 | 9,700

| 45,500 | 127,000

| 525,000

|

June 3

| 197

| 2,550 | 8,470

| 42,500 | 122,000

| 471,000

|

June 1

| 216

| 2,540 | 8,370

| 42,000 | 122,000

| 466,000

|

May 30

| 225

| 2,530 | 7,990

| 41,600 | 121,000

| 428,000

|

May 28

| 217

| 2,480 | 7,870

| 41,100 | 119,000

| 420,000

|

May 26

| 225

| 2,390 | 7,590

| 41,600 | 119,000

| 420,000

|

May 24

| 224

|

|

7,470

|

|

120,000

| 420,000

|

May 22

| 223

|

|

7,300

|

|

117,000

| 409,000

|

May 20

| 196

|

|

7,040

|

|

111,000

| 403,000

|

May 18

| 193

|

|

7,135

|

|

110,000

| 406,000

|

May 16

| 180

|

|

7,125

|

|

111,000

| 396,000

|

May 14

| 174

|

|

7,025

|

|

109,000

| 381,000

|

May 12

| 189

|

|

6,850

|

|

105,000

| 386,000

|

May 10

| 222

|

|

6,900

|

|

116,000

| 393,000

|

May 8

| 183

|

|

6,860

|

|

119,000

| 339,000

|

May 6

| 202

|

|

6,475

|

|

103,000

| 352,000

|

May 4

|

200

|

|

6,000

|

|

95,000

|

386,000

|

May 2

|

205

|

|

5,900

|

|

117,000

|

380,000

|

Apr 30 2020

|

238

|

|

5,120

|

|

80,000

|

380,000

|

Apr 28 forecasts

for June 21st 2020

|

176

|

|

3,960

|

|

70,500

|

314,000

|

TRUMP-VIRUS THRUST USA ECONOMY into TECHNICAL RECESSION in MARCH 2020

Dec 18th 2021 update - So how did the USA embark on this historic

crisis? Here's a clue: During a White House Rose Garden

virtual town hall on March 25th 2020, the President stated to the Fox

News host:

"You'll

have packed churches all over the country. It would be a

resurrection of biblical proportions. I would love to have the

country opened up and raring to go by Easter. It would be a

beautiful thing. "Our country has to get back to work, otherwise it's

going to be very hard to start it up again. We can't lose the

advantage we have."

It was on this precise day America

was infected with "the TrumpVirus". On that day the USA had

only 4% of global Covid deaths - apropos considering the nation has 4% of the

world's population.

But it marked the day everything

changed. And leads one to ask why does the USA have 23%

of world's cumulative Covid

cases, 56% of the today's global "active" cases & 24% of worldwide body bags? The answer is founded in its

citizenry electing

a reality show celebrity as its President. This business con man's failure to

mitigate Covid-19's spread runs the length of his stay in office.

Albeit Obama's Homeland Security

Chief (Lisa Monaco) briefed the incoming transition team with a robust

"playbook", un-indicted Individual-1 shut down the White House's

National Security Council's Pandemic Unit in 2018. Dr Dennis

Carol's Predict Program was cancelled by the White House in 2019.

And 'cuz their very public warnings were rocking the stock markets in

Feb/2020, CDC's renowned disease experts Sarah Messonnier & Dr

Bright were abruptly reassigned.

This prudent planning team was replaced by a muse "this flu will just go

away with warm April sunshine". After his "miracle"

failed, the self-proclaimed "extremely stable genius" offered his cult following hydroxychloroquine, disinfectant injections and internal UV light

remedies.

It was soon evident many continued to

drink the

Kool-Aid (or bleach?). Prior to flattening their curves, mostly

"red States" relaxed physical distancing, stay-at-home policies, masking &

contact tracing.

From the onset it was evident Trump's "Opening Up

America Again"

campaign was rooted in politics. Despite

his bravado, to that point in time he failed to attain Obama's multiple

5% GDP growth rates. 2020's Q1/Q2/Q3 were his last-kick-at-the-can

- hence his nonsensical dampened pandemic rhetoric thru January,

February & March. With Q1 going negative (-5%), he knew a large part

of his Nov/2020 Election demise rested on Q2 & Q3 GDP.

So the

motive for his March 25th plea (above) for Easter church goers to

return to work April 14th is clear. As a ratings savvy guy, he

knew Q2 GDP (for Apr/May/June) would be

announced in late July (with Aug27th & Sept30th revisions). The Q3

GDP announcement was Oct29th - a mere five days prior to Election Day (Nov3rd).

And

evidently, he's in huge trouble for failing to contain Covid-19.

The uncontained TrumpVirus resulted in GDP crashing at a historic -31%

pace in Q2. And of

the 75 million workers initiating unemployment claims due to the pandemic during his term, 2.5

million remain on the rolls (1.7 mil pre-pandemic). With no sign of his boasted

V-shaped

Recovery, Individual-1 tried some desperate manoeuvres ... like forcing

schools to

re-open ... attempting to postpone the Election ... sabotaging the

postal system for an

electoral advantage ... and challenging those mail-in ballots and

finally ... recruiting nationalist militia to overthrow the Capitol on

January 6th.

The President caused a TrumpVirus resurgence only for the purpose of salvaging his legacy. He

desperately wanted to avoid voters going to the polls realizing The Donald (alone)

was at fault for April's 22% U-6 Unemployment Rate & plunging

the U.S. economy into its deepest crash (-31% GDP) ever - including the Great Depression.

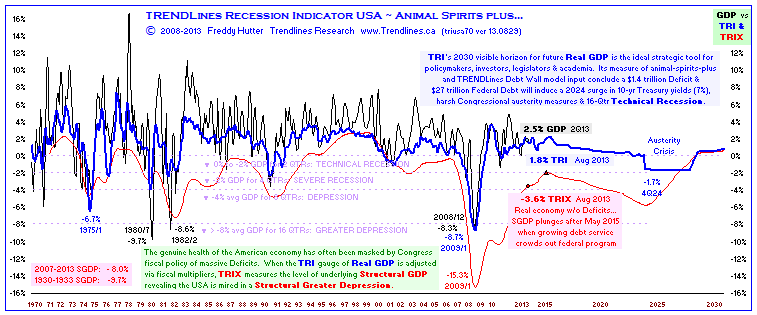

The TRENDLines

Recession Indicator was the

first macro-economic model to accurately reveal the magnitude of the Great Recession in real

time. In the 2013 chart below, TRI was forecasting a USA austerity

crisis to occur in

2024 due to an uncontrolled $26 trillion National Debt. But that

day was pre-empted by a black swan event: the TrumpVirus - a

crisis of epic proportions in mismanagement, lack of containment &

mitigation failures - resulting in 815,000 fatalities (thus far).

Despite interventions by the Federal Reserve via its monetary policy tool

box and fiscal policy injections of trillions of dollars by Congress, it

is probable the American economy will suffer long-term

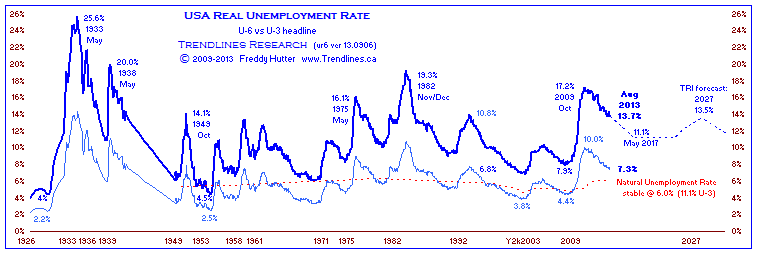

consequences. April's "real" Unemployment Rate (U-6) of 22%

was the worst since the 26% high (1933) in the Great Depression (see

chart below). Q2GDP plunged 31% (annualized rate), dwarfing the 2008 & 1980

downturns and anything seen in the great Depression.

the traditional definitions

TECHNICAL RECESSION:

Avg Gross Domestic Product growth rate (GDP) declines 0% to 2% for at

least 2 Quarters within an environment of rising unemployment.

SEVERE RECESSION: Avg GDP declines 2% to 4% for at least 4 Qtrs (1 yr)

DEPRESSION: Avg GDP declines 4% to 8% for at least 8 Qtrs (2 yrs)

GREATER DEPRESSION: Avg GDP declines over 8% for at least 16 Qtrs (4 yrs)

RECOVERY PERIOD: monthly/quarterly nominal GDP expanding but remains below pre-contraction peak

EXPANSION PERIOD: monthly/quarterly nominal GDP finally exceeds pre-contraction peak

STRUCTURAL GDP (TRIX): Real GDP adjusted for Fiscal Policy Deficit/Surplus effects to reveal growth rate of underlying economy

UPPER CLASS: family wealth (net worth) is among the top 1% of society

MIDDLE CLASS: family income is among the top 10% of society

WORKING CLASS: all the rest...

U-6 UNEMPLOYMENT RATE:

Marginally attached workers are persons who currently are neither

working nor looking for work but indicate that they want and are

available for a job and have looked for work sometime in the recent

past. Discouraged workers a subset of marginally attached,

have given a job-market related reason for not looking currently for a

job. Persons employed part time for economic reasons are those who

want and are available for full-time work but have had to settle for a

part-time schedule.

|

|

|

|

| START

FINISH

|

|

|

|

|

|

|

~

send

email to

Freddy Hutter

with questions, comments or navigation corrections with respect to

this web site

~

Last modified: May 8 2023

~ (© 1989-2023 TRENDLines Research)

|

|

keywords: projection prediction forecast indicate guess estimate how many people will

die perish in bc british columbia canada canadians usa

americans united states globe world worldwide earth result from corona virus covid-19

pandemic flu death toll daily total cumulative fatalities perish

victims trendlines freddy hutter CDC IHME model pplm post-peak

linearization social physical distancing

|

|

|

|

TRENDLines Research's

YUKON PROTOCOL

for the UN's

CLIMATE FINANCE DELIVERY PLAN

& its GREEN CLIMATE FUND

Nov 24th 2021 - TRENDLines

Research published its "Yukon Protocol" on Aug 23 2009 to provide guidance to the UNFCCC (United Nations Framework Convention on Climate Change)

and policymakers of developed nations in establishing equitable

contributions wrt the $100 billion Climate Finance Delivery

Plan -- reaffirmed at COP26-Glasgow-2021.

As background, after each of the UN's IPCC (Intergovernmental Panel on Climate Change) reports,

developing nations begrudged demands on them to forego economical coal, oil and gases as their gracious part in "saving the planet".

Their objections are founded in

the perceived

unfairness that while today's wealthy nations achieved their status in

part via industrialization under a high emissions regime, the latter has

undergone an epiphany of sorts and so to suppress imminent climate

change due to past sins, they now chastise developing nations for

utilizing those same efficient fossil fuel resources to foster their

growth.

So as a fairness measure to offset

the cost burden of low emission infrastructure in young economies,

COP15-Copenhagen-2009 proposed a Green Climate Fund (GCF) from which

they can draw upon -- and to be funded by mature nations.

Subsequent COP's (Conference Of the Parties) established the GCF, but a dozen years on, donor nations continue a struggle to find equitable contribution levels.

TR's Yukon Protocol suggests a

truly relevant apportionment of the $100 billion Climate Finance

Delivery Plan rests in setting national contributions in accordance to

each country's share of cumulative co2 emissions.

The

Yukon Protocol's latest methodology divides up the $100 billion Climate

Finance target among the top 100 co2 emitters using their known prorated

share of cumulative emissions (since Year 1750). Said 100 are

responsible for 97% of total emissions for this period. The

remaining 114 nations are candidates for GCF grants & loans.

With full compliance, annual contributions within the Protocol range from $31 million assessed against Jamaica - the

lowest of the 100 top emitters (0.03%) to $25.65 billion due from

the largest - the USA (25.65%). Over 2/3 of the target is achieved levying the top ten emitters.

Credit to CDIAC, GCP & OWID acknowledged as data sources.

link to 5pg printable PDF

YUKON PROTOCOL FOR CLIMATE FINANCE

DELIVERY PLAN

|

Top 100

emitter nations

|

funding proportion based on cumulative co2 emissions

|

assessed share of

$100 billion target

|

emitter rating

|

|

|

|

|

|

|

United

States

|

25.65%

|

$25,651,095,494

|

1

|

|

China

|

13.76%

|

$13,755,684,167

|

2

|

|

Russia

|

7.12%

|

$7,120,711,038

|

3

|

|

Germany

|

5.75%

|

$5,746,176,106

|

4

|

|

United

Kingdom

|

4.87%

|

$4,867,713,931

|

5

|

|

Japan

|

4.04%

|

$4,040,926,002

|

6

|

|

India

|

3.25%

|

$3,245,142,621

|

7

|

|

France

|

2.39%

|

$2,387,350,145

|

8

|

|

Canada

|

2.07%

|

$2,066,969,822

|

9

|

|

Ukraine

|

1.85%

|

$1,849,937,991

|

10

|

|

Poland

|

1.73%

|

$1,725,919,802

|

11

|

|

Italy

|

1.52%

|

$1,519,222,819

|

12

|

|

South

Africa

|

1.29%

|

$1,291,856,139

|

13

|

|

Mexico

|

1.24%

|

$1,240,181,893

|

14

|

|

Iran

|

1.15%

|

$1,147,168,251

|

15

|

|

Australia

|

1.14%

|

$1,136,833,402

|

16

|

|

South

Korea

|

1.06%

|

$1,064,489,458

|

17

|

|

Brazil

|

0.95%

|

$950,806,118

|

18

|

|

Saudi

Arabia

|

0.93%

|

$930,136,420

|

19

|

|

Spain

|

0.92%

|

$919,801,571

|

20

|

|

Indonesia

|

0.85%

|

$847,457,627

|

21

|

|

Kazakhstan

|

0.84%

|

$837,122,778

|

22

|

|

Belgium

|

0.78%

|

$775,113,683

|

23

|

|

Czechia

|

0.74%

|

$744,109,136

|

24

|

|

Netherlands

|

0.72%

|

$723,439,438

|

25

|

|

Turkey

|

0.65%

|

$651,095,494

|

26

|

|

Taiwan

|

0.54%

|

$537,412,154

|

27

|

|

Romania

|

0.53%

|

$527,077,305

|

28

|

|

Argentina

|

0.52%

|

$516,742,456

|

29

|

|

Venezuela

|

0.49%

|

$485,737,908

|

30

|

|

Thailand

|

0.44%

|

$444,398,512

|

31

|

|

Uzbekistan

|

0.41%

|

$413,393,964

|

32

|

|

Egypt

|

0.38%

|

$382,389,417

|

33

|

|

Malaysia

|

0.36%

|

$361,719,719

|

34

|

|

Austria

|

0.34%

|

$341,050,021

|

35

|

|

Belarus

|

0.33%

|

$330,715,172

|

36

|

|

North

Korea

|

0.32%

|

$320,380,322

|

37

|

|

Hungary

|

0.31%

|

$310,045,473

|

38

|

|

Pakistan

|

0.31%

|

$310,045,473

|

38

|

|

Sweden

|

0.31%

|

$310,045,473

|

38

|

|

United

Arab Emirates

|

0.29%

|

$289,375,775

|

41

|

|

Algeria

|

0.28%

|

$279,040,926

|

42

|

|

Iraq

|

0.28%

|

$279,040,926

|

43

|

|

Denmark

|

0.26%

|

$258,371,228

|

44

|

|

Greece

|

0.25%

|

$248,036,379

|

45

|

|

Bulgaria

|

0.24%

|

$237,701,530

|

46

|

|

Nigeria

|

0.24%

|

$237,701,530

|

46

|

|

Slovakia

|

0.24%

|

$237,701,530

|

46

|

|

Vietnam

|

0.23%

|

$227,366,680

|

49

|

|

Colombia

|

0.21%

|

$206,696,982

|

50

|

|

Philippines

|

0.21%

|

$206,696,982

|

50

|

|

Finland

|

0.20%

|

$196,362,133

|

52

|

|

Switzerland

|

0.19%

|

$186,027,284

|

53

|

|

Chile

|

0.18%

|

$175,692,435

|

54

|

|

Kuwait

|

0.18%

|

$175,692,435

|

54

|

|

Serbia

|

0.18%

|

$175,692,435

|

54

|

|

Azerbaijan

|

0.17%

|

$165,357,586

|

57

|

|

Norway

|

0.17%

|

$165,357,586

|

57

|

|

Portugal

|

0.17%

|

$165,357,586

|

57

|

|

Turkmenistan

|

0.17%

|

$165,357,586

|

57

|

|

Israel

|

0.14%

|

$144,687,888

|

61

|

|

Ireland

|

0.13%

|

$134,353,038

|

62

|

|

Singapore

|

0.13%

|

$134,353,038

|

62

|

|

Libya

|

0.12%

|

$124,018,189

|

64

|

|

Qatar

|

0.12%

|

$124,018,189

|

64

|

|

New

Zealand

|

0.11%

|

$113,683,340

|

66

|

|

Peru

|

0.11%

|

$113,683,340

|

66

|

|

Syria

|

0.11%

|

$113,683,340

|

66

|

|

Cuba

|

0.10%

|

$103,348,491

|

69

|

|

Hong

Kong

|

0.10%

|

$103,348,491

|

69

|

|

Morocco

|

0.10%

|

$103,348,491

|

69

|

|

Bangladesh

|

0.09%

|

$93,013,642

|

72

|

|

Estonia

|

0.09%

|

$93,013,642

|

72

|

|

Trinidad

& Tobago

|

0.09%

|

$93,013,642

|

72

|

|

Lithuania

|

0.08%

|

$82,678,793

|

75

|

|

Croatia

|

0.07%

|

$72,343,944

|

76

|

|

Ecuador

|

0.07%

|

$72,343,944

|

76

|

|

Oman

|

0.07%

|

$72,343,944

|

76

|

|

Bosnia

& Herzegovina

|

0.06%

|

$62,009,095

|

79

|

|

Georgia

|

0.06%

|

$62,009,095

|

79

|

|

Moldova

|

0.06%

|

$62,009,095

|

79

|

|

Bahrain

|

0.05%

|

$51,674,246

|

82

|

|

Kyrgyzstan

|

0.05%

|

$51,674,246

|

82

|

|

Latvia

|

0.05%

|

$51,674,246

|

82

|

|

Luxembourg

|

0.05%

|

$51,674,246

|

82

|

|

Slovenia

|

0.05%

|

$51,674,246

|

82

|

|

Tunisia

|

0.05%

|

$51,674,246

|

82

|

|

Zimbabwe

|

0.05%

|

$51,674,246

|

82

|

|

Angola

|

0.04%

|

$41,339,396

|

89

|

|

Armenia

|

0.04%

|

$41,339,396

|

89

|

|

Dominican

Republic

|

0.04%

|

$41,339,396

|

89

|

|

Jordan

|

0.04%

|

$41,339,396

|

89

|

|

Lebanon

|

0.04%

|

$41,339,396

|

89

|

|

Mongolia

|

0.04%

|

$41,339,396

|

89

|

|

North

Macedonia

|

0.04%

|

$41,339,396

|

89

|

|

Yemen

|

0.04%

|

$41,339,396

|

89

|

|

Bolivia

|

0.03%

|

$31,004,547

|

97

|

|

Curacao

|

0.03%

|

$31,004,547

|

97

|

|

Guatemala

|

0.03%

|

$31,004,547

|

97

|

|

Jamaica

|

0.03%

|

$31,004,547

|

97

|

|

|

100.00%

|

|

assessed nations:

|

|

ver 21.1116

|

100.00%

|

$100,000,000,000

|

100

|

|

|

|

|

|

|

|

|

|

|

|

114

Recipient Entities:

|

|

|

|

|

|

|

|

|

|

Kenya

|

|

|

|

|

Myanmar

|

|

|

|

|

Sri

Lanka

|

|

|

|

|

Sudan

|

|

|

|

|

Tajikistan

|

|

|

|

|

Albania

|

|

|

|

|

Brunei

|

|

|

|

|

Cote

d'Ivoire

|

|

|

|

|

Cyprus

|

|

|

|

|

Gabon

|

|

|

|

|

Ghana

|

|

|

|

|

Honduras

|

|

|

|

|

Panama

|

|

|

|

|

Uruguay

|

|

|

|

|

Afghanistan

|

|

|

|

|

Bahamas

|

|

|

|

|

Benin

|

|

|

|

|

Botswana

|

|

|

|

|

Cambodia

|

|

|

|

|

Cameroon

|

|

|

|

|

Costa

Rica

|

|

|

|

|

Democratic

Republic of Congo

|

|

|

|

|

El

Salvador

|

|

|

|

|

Equatorial

Guinea

|

|

|

|

|

Ethiopia

|

|

|

|

|

Guyana

|

|

|

|

|

Iceland

|

|

|

|

|

Kosovo

|

|

|

|

|

Laos

|

|

|

|

|

Madagascar

|

|

|

|

|

Malta

|

|

|

|

|

Mauritius

|

|

|

|

|

Montenegro

|

|

|

|

|

Mozambique

|

|

|

|

|

Nepal

|

|

|

|

|

New

Caledonia

|

|

|

|

|

Nicaragua

|

|

|

|

|

Papua

New Guinea

|

|

|

|

|

Paraguay

|

|

|

|

|

Senegal

|

|

|

|

|

Suriname

|

|

|

|

|

Tanzania

|

|

|

|

|

Uganda

|

|

|

|

|

Zambia

|

|

|

|

|

Andorra

|

|

|

|

|

Anguilla

|

|

|

|

|

Antigua

& Barbuda

|

|

|

|

|

Aruba

|

|

|

|

|

Barbados

|

|

|

|

|

Belize

|

|

|

|

|

Bermuda

|

|

|

|

|

Bhutan

|

|

|

|

|

Bonaire

Sint Eustatius & Saba

|

|

|

|

|

British

Virgin Islands

|

|

|

|

|

Burkina

Faso

|

|

|

|

|

Burundi

|

|

|

|

|

Cape

Verde

|

|

|

|

|

Central

African Republic

|

|

|

|

|

Chad

|

|

|

|

|

Comoros

|

|

|

|

|

Congo

|

|

|

|

|

Cook

Islands

|

|

|

|

|

Djibouti

|

|

|

|

|

Dominica

|

|

|

|

|

Eritrea

|

|

|

|

|

Eswatini

|

|

|

|

|

Faeroe

Islands

|

|

|

|

|

Fiji

|

|

|

|

|

French

Polynesia

|

|

|

|

|

Gambia

|

|

|

|

|

Greenland

|

|

|

|

|

Grenada

|

|

|

|

|

Guinea

|

|

|

|

|

Guinea-Bissau

|

|

|

|

|

Haiti

|

|

|

|

|

Kiribati

|

|

|

|

|

Lesotho

|

|

|

|

|

Liberia

|

|

|

|

|

Liechtenstein

|

|

|

|

|

Macao

|

|

|

|

|

Malawi

|

|

|

|

|

Maldives

|

|

|

|

|

Mali

|

|

|

|

|

Marshall

Islands

|

|

|

|

|

Mauritania

|

|

|

|

|

Micronesia

|

|

|

|

|

Montserrat

|

|

|

|

|

Namibia

|

|

|

|

|

Nauru

|

|

|

|

|

Niger

|

|

|

|

|

Niue

|

|

|

|

|

Palau

|

|

|

|

|

Palestine

|

|

|

|

|

Rwanda

|

|

|

|

|

Saint

Helena

|

|

|

|

|

Saint

Kitts & Nevis

|

|

|

|

|

Saint

Lucia

|

|

|

|

|

Saint

Pierre & Miquelon

|

|

|

|

|

Saint

Vincent & Grenadines

|

|

|

|

|

Samoa

|

|

|

|

|

Sao

Tome & Principe

|

|

|

|

|

Seychelles

|

|

|

|

|

Sierra

Leone

|

|

|

|

|

Sint

Maarten (Dutch)

|

|

|

|

|

Solomon

Islands

|

|

|

|

|

Somalia

|

|

|

|

|

South

Sudan

|

|

|

|

|

Timor

|

|

|

|

|

Togo

|

|

|

|

|

Tonga

|

|

|

|

|

Turks

& Caicos Islands

|

|

|

|

|

Tuvalu

|

|

|

|

|

Vanuatu

|

|

|

|

|

Wallis

& Futuna

|

|

|

|

|

|

About TRENDLines Research

Data analyst Freddy Hutter of Vancouver Island BC has developed models

& methodologies for macro-economic charts & guidance for

policy-makers, stakeholders. legislators, investors, educators, and the public with a

long term multi-disciplinary perspective since 1989. TRENDLines

removes the noise in (economic) data to reveal the underlying

trends. Specialties

include: Recession Indicators for Canada, USA & China;

Realty Bubble Indicators for Canada, USA, UK & Australia;

Global Oil Production & Price Component analysis/forecasts;

& national, provincial Party & Presidential political election

projections. Covid-19 ultimate deaths forecasting is the most recent endeavour.

|

|

|

|

|

~

-

the FreeVenue

chart-of-the-day is a public posting of guidance (charts, tables

& analysis)

-

Trendlines

Research has been publishing charts & analysis relating to Peak

Oil, Macro-Economics, Climate Change & Political Election

Projections since 1989. Data analyst Freddy Hutter's media

and professional commentary on these issues commenced in 1973

- all charts, tables & text © 1989-2021 all rights reserved TRENDLines Research

|

~ |

|

|

|

|

|

|

clik to follow @TrendlinesDotCa for new chart alerts |

|

|

|